Better-Pro Architecture Layer

Better-Pro is the go-to platform for trading all assets, including cryptocurrencies, forex, com-modities, and indices, with up to 500x leverage. Better-Pro supports EVM blockchains andintegrate smart wallets.

Better-Pro has three layers to : pricing layer, position opening and position closing. To fully understand these layers, we need to understand perpetuals. Mathematically, a perpetual futures written on an underlying price process (St)∞ 0 is an agreement between the long and the short side. There is zero cost to enter the agreement. After entering, both the long side and the short side can terminate the contract at any time t. There are two important rules to remember:

• Payoff at the termination of contract: At time t, if one of the two sides decide to terminate the contract, then the short needs to pay the long Ft − F0 for each unit shorted, where (Ft)∞ 0 denotes the price process of the perpetuals.

• To keep the futures price Ft close to spot price St, there is a mechanism called Funding Rate, where the long has to pay the short a rate that is proportional to Ft − St. This rate is revised periodically, usually 8 hours. From an arbitrageur point of view, if Ft >> St, he will take the short position with the hope that the price will later on reverse to St to realize a profit.

There will be two sources of profit for him: the funding rate Ft − St, and the terminal payment Ft − FT paid by the long side. Despite such economical soundness, unlike fixed-maturity futures, perpetuals are not guaranteed to converge to the spot price of their underlying asset at any time. The reason is clear: there is no hard no-arbitrage argument available for perpetuals like fixed-maturity futures.

Pricing layer Dynamic price feed (DPF).

This is a key component in ensuring accurate pricing for all assets tradedon the platform. The DPF algorithm is designed to calculate an accurate average price for all assets onthe platform. This is achieved by collecting data from multiple sources, including external oracles andcentralise trading data. By incorporating multiple data sources, the DPF helps to minimize the impact oincorrect oracle values or trading anomalies.

This helps to ensure that the pricing data is as accurate andreliable as possible. Note that we do not use any on-chain service such as Chainlink, but rather create ourown centralized price oracles.

Plexible market making.

Better-ProFlexible Market Making (FMM) model is inspired bythe DoDo Proactive Market Making model. The essential idea is to use oracle price as the reference price(or mark price), and linear price slippage, i.e. price impact is proportional to the trading volume.

Moreprecisely, assume that we have a buy order of size ATo, LnP=B(1+R),R=a-20

where P denotes the initial mark price, given by an oracle price, and P denotes the updated mark price.R denotes the price return of the transaction. R is a linear function of the relative trading size A-.

Theconstant a denotes the liquidity concentration ratio.

For example, if a= 0.1 and the mark price is $100then the entire liquidity will be approximately concentrated in the price interval $95, $105 with flat density.

The slippage will be equal to ei220 The FMM model is different from the PMlM model in that, it does not have an absolute inventory control byadjusting the reference price based on the reserves inventory z - rin tia. However, by allowing the slip.page to be a function of the relative position size, the model can somewhat controls the relative inventoryratio, i.e. the value proportion of one token in the pool, which is good enough in practice.

Position opening layer

When a long/short position is created, the mark price is given by the oracle (Dynamic Price Feed). Depending on the asset class and the collateral asset value, a position size will be determined. A priceslippage will be calculated based on the relative position size. Finally, the average transaction price canbe calculated based on slippage and mark price.

Position closing layer

When a long/short position is closed, there will be two cases, either the position is liquidated or not. lfthere is no liguidation, then the calculation will be similar to the position closing case, except that a PnLsetlement has to be calculated. if liguidation takes place, an amount of collateral will be liquidated andliquidator can request liquidation fee from the trading storage.

An exciting feature of Better-Pro is to allow traders use limit, profit-taking and stop-lossorders. Regarding automated execution, whenever the taking-profit or stop-oss thresholds and marketprices are met, the trading service will take a portion of the collateral asset to cover for the PnL of thetrades, and send the leftover to users.

DeFutures Vaults

One of the defining feature of GMX is that, the protocol utilizes a unique multi-asset liauidity pool thatdeviates from the traditional models of multinle sinale-asset pools. This feature is no longer retained in ourmodel.

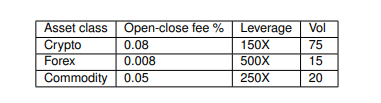

Just like Gains Network, in Better-Pro, not only crypto currencies are traded, but also tokenized realworld assets such as currencies, and commodities (OlL and GOLD) are also traded. Each asset class(such as crypto, forex and commodities) has a different price volatility, or different risk contribution to thetotal portfolio. Therefore, they should be treated differently in terms of trading fees and leverage (or marginrequirement or liquidation requirement). For instant, crypto assets are much volatile than forex currencies hence forex leverage should be much larger than crypto leverage, and forex trading fees should be smallerthan crypto trading fees. This is the main reason why DeFutures assets are split into three different vaults

Better-Pro Vault is a core function in our architecture, with the main functions of split the trading feesand allow traders to earn great yields on them. Additionally, Better-Pro Vault has the potential for futuretoken drops.

Copy trading

Better-Pro Bot feature will allow users to easily follow and copy the trades of experiencedtraders on our Better-Pro. By monitoring the performance of a wide range of traders on ouplatform, users can choose to automatically replicate the trades of top-performing traders with just a fewclicks.

This feature not only makes it eas ier for novice traders to enter the market and potentially make profitable trades, but also allows experienced traders to increase their earnings by sharing their tradingstrategies and insights with others.The most interesting feature is Smart Vault Trading: Copy Trades using ERC-4337 Smart Contract Wallet.

Copy trading is just a middle step in the phase of building a decentralized hedge fund [Nam to discuss].By combining the zkSync technology and Al, fund managers can create their own trading bots with highout-of-sample trading performance without revealing their strategies to the outside world. As trading botscan be ranked and compared, traders can allocate capital to the bots they prefer, and this open newpossibilities for passive income on blockchain.

LP insurance

The most crucial question that any perpetual futures exchange has to answer is whether or not they should hedge the LPs’ position. Apparently, there are two extremes.

First, no hedging at all. This sounds counter intuitive, but the fact is that most of the time traders loose and the exchange win as they take the opposite position. Therefore, no hedging will be the best solution most of the time. However, this solution is really risky if traders have private information.

Second, hedging all the time to ensure delta neutral. This solution is impossible because the cost of hedging will very quickly outweigh the gain from trading fees.

A middle way solution is to do partial hedging. There are many delta-netral hedging strategies to protect LPs in GMX with infrequent hedges but still guarantee low impermanent loss. These strategies are implemented by third parties, so it is up to LPs to choose hedging strategies for themselves. This will be the solution for the current moment for Better-Pro.

In this whitepaper, we propose an LP insurance solution via selling put options in a periodic manner. This solution will be implemented in the near future. The brief idea is as follows. We create an Insurance pool so that policy sellers can mint put options and deposit collaterals for those options. Put options expire monthly, it has as many strikes as policy sellers wish to mint. An LP can send a buying request at any time to the insurance pool, and insurance pool can mint the option of interest to the LP.

So how can an option be priced? We apply the Black-Scholes model to have

The most important parameter that needs to be priced is the implied volatility. We assume a to be constantacross different strikes and maturities. lf we denote t, as the utilization ratio of options nominal, or thetotal option demand devided by total option supply, and g: as the gain rate of a representative option sellerthen the implied volatility can be expressed as follows

Where F is an increasing function. The equation means that if [ increases, i.e. there is more demand ofput options, then the implied vol will increase to make it more expensive and vice version. More interest.ingly, when gt > 0, i.e. options seller gains more than looses by selling options, the exponential decay will make implied volatilitly cheaper, thus put options become cheaper and gain rate of option sellers will be lower.

Real Yield calculation

Crypto real yield as a metric compares a project's offered yield against its revenue. lf the returns forstaking are greater in real terms than the provided interest, the emissions are dilutionary. This meansthat their yield isn't sustainable or, in lay terms, "real." Real yield isn't necessarily better than dilutionaryemissions, which are often used for marketing purposes. However, this indicator can serve as a useful toofor gauging a project's long-term yield-bearing prospects. Real yield is generated from revenue sources instead of token emissions.